Market Update

Quarter Ending March 31, 2025

Quick Hits

- Challenging Start to the Year for Stocks

- Solid Quarter for Bonds

- Economic Update

- Market Risks Worth Monitoring

- Cautiously Optimistic Outlook

Challenging Start to the Year for Stocks

It was a rough March for stocks, capping off a weak quarter to start the year. The S&P 500 lost 5.63 percent in March and 4.27 percent in the first quarter. The Dow Jones Industrial Average was down 4.06 percent during the month and 0.87 percent for the quarter. The Nasdaq Composite lagged its peers during the month and quarter, with an 8.14 percent loss in March and a 10.26 percent drop for the quarter. Technology and growth stocks experienced higher levels of volatility to start the year on concerns surrounding AI and valuations.

Despite the poor performance, fundamental factors showed signs of improvement. Per Bloomberg Intelligence, as of March 31 with all companies having reported earnings, the average earnings growth rate for the S&P 500 in the fourth quarter was 14.3 percent. This is notably higher than analyst estimates at the start of earnings season for a more modest 7.3 percent increase. The better-than-expected earnings growth was widespread as each of the 11 sectors ended the quarter above analyst estimates. Over the long run, fundamentals have driven market performance, so the impressive earnings growth was a good sign for investors.

While fundamental factors were supportive for the quarter, technical factors were another story. All three major U.S. indices ended March below their respective 200-day moving averages. (The 200-day moving average is a widely monitored technical indicator as sustained breaks above or below this level can signal shifting investor sentiment for an index.) The drop below trend in March for each of these indices is worth monitoring given the previous technical support that each of these indices received throughout 2024 and the start of 2025. If we continue to see these indices remain below trend for several months, it could signal souring investor confidence in U.S. equities.

International stocks had a better start to the year, despite a mixed March. The MSCI EAFE Index fell 0.40 percent in March but still managed a 6.86 percent gain for the quarter. The MSCI Emerging Markets Index was up 0.67 percent in March and 3.01 percent for the quarter. Improving fundamentals and rising expectations for government spending and stimulus helped support international stock returns to start the year. Technical results were mixed for international stocks, as the MSCI EAFE Index ended the month above its 200-day moving average, while the MSCI Emerging Markets index fell below trend at the end of March.

Solid Quarter for Bonds

While equities had a largely negative start to the year, results were more encouraging for fixed income investors. Falling interest rates throughout the quarter led to rising bond prices and positive returns for most fixed income sectors. The 10-year U.S. Treasury yield fell from 4.58 percent at the end of 2024 to 4.23 percent at the end of March. The Bloomberg U.S. Aggregate Bond Index gained 0.04 percent for the month and a strong 2.78 percent for the quarter.

High-yield fixed income, which is typically less sensitive to changing interest rates, was a bit more mixed. The Bloomberg U.S. Corporate High Yield Index lost 1.02 percent in March yet managed a 1.00 percent return for the quarter. High-yield credit spreads started the year at 2.92 percent and ended March at 3.55 percent. Rising credit spreads are a sign that investors became more cautious during the quarter and required additional yield to invest in lower-credit quality bonds.

Solid Economic Environment for Now

The economic updates released throughout the quarter showed signs of solid economic growth to start the year. Hiring accelerated to end 2024 and that momentum has carried over into 2025. A healthy 151,000 jobs were added in February, and the unemployment rate remained relatively low at 4.1 percent. This continued job growth helped support personal income and spending growth, which rebounded in February after pulling back modestly in January.

Business spending was also supportive in the first quarter. Core durable goods orders, which are often viewed as a proxy for business investment, rose by 0.7 percent in February. This was well above economist estimates and indicates that businesses continued to invest to start the year despite the market turbulence.

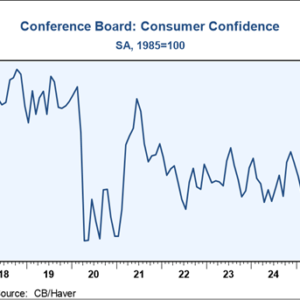

While the hard data was largely positive in the first quarter, there are some signs of potential weakness ahead. Consumer confidence declined throughout the quarter, due in large part to rising political uncertainty and inflation expectations. Large drops in confidence have been associated with slower spending and economic growth in the future, so the notable decline in confidence to start the year is a risk that investors should monitor.

Figure 1: Conference Board Consumer Confidence March 2018–Present

Source: CB/Haver, as of March 25, 2025.

The Takeaway

- Economic growth continued throughout the quarter, with solid hiring growth leading the way.

- Consumer and business spending were healthy in February.

- Worsening consumer confidence to start the year is a potential risk to future spending and economic growth.

Market Risks Worth Monitoring

While a healthy economic backdrop and strong fundamentals were encouraging developments for long-term investors to start the year, the market volatility served as a reminder that real risks remain for investors. The falling consumer confidence throughout the quarter is a potential risk to the economic outlook given the importance of consumer spending on overall economic growth.

Asides from economic concerns, political uncertainty remains another large risk for markets. The planned rollout of tariffs continues to cause uncertainty and contributed to the rattled markets at the start of the year.

International risks remain as well, highlighted by the continued conflicts in Ukraine and the Middle East. And, as always, markets continue to face unknown risks that could pop up at any time. There’s certainly a lot for investors to keep an eye on. Given the real risks that markets face, it’s quite possible that we’ll see continued choppy returns in the months ahead.

The Takeaway

- Risks remain for markets, including economic and political risks.

- Domestic risks include a potential economic slowdown as well as high levels of political uncertainty.

- Unknown risks can also negatively impact markets and can’t be predicted.

Cautiously Optimistic Outlook

While it’s certainly important to acknowledge the current market risks, on balance we believe we remain in a relatively good place.

The economic backdrop remains largely supportive, powered by a resilient job market and decent spending in the first quarter. U.S. companies have shown an impressive ability to grow earnings, and analysts expect to see continued earnings growth in the quarters ahead. Despite the recent turbulence, it’s important to note that bouts of short-term volatility are normal when investing over the long term. While negative quarters can feel painful for investors at the time, over the long run, the outlook remains cautiously optimistic.

Ultimately, things are pretty good right now, but that may not always be the case. While continued economic growth and market appreciation remain the most likely path forward, we may face short-term setbacks along the way. Given the potential for short-term uncertainty, a well-diversified portfolio that matches investor goals with timelines remains the best path forward for most. If concerns remain, you should speak to your financial advisor about your financial plans.

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

Authored by Chris Fasciano, chief market strategist, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

© 2025 Commonwealth Financial Network®

Resources for You

Webinars

Expand your financial literacy with valuable webinars developed by our experts. Learn about asset management, financial planning, and more.

Videos

Watch our videos to help get you started on your journey toward financial freedom. Learn actionable tips for responsible investing and insurance.

Calculators

Use our calculators to make informed decisions about your investments, retirement savings, automotive loans, mortgage, and personal finances.